Merchant Onboarding & Know-Your-Business (KYB) Requirements

Merchant Onboarding & Know-Your-Business Requirements Merchant onboarding is a critical function for EPSPs that operate payment acceptance services, POS terminals, or payment gateway solutions. To prevent misuse of digital payment channels, EPSPs must conduct due diligence on merchants through Know-Your-Business (KYB) checks. These checks verify that merchants are legitimate, licensed, and engaged in lawful activities. Merchant Onboarding Requirements Collection of business registration documents Verification of licensing and commercial activities Risk classification of merchant industry Assessment of transaction patterns and expected volumes Beneficial ownership identification Operational Controls Chargeback and refund procedures Pricing transparency and fee disclosures Merchant reporting dashboards Settlement scheduling and bank account verification CBI compliance Conduct KYB in accordance with AML/CFT guidelines Monitor merchant transactions for unusual behavior Report suspicious merchant activity where applicable Maintain merchant files for audit and supervisory review How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

ESG Standards Guidance for 2025

ESG Standards Guidance for 2025 The shift toward Environmental, Social, and Governance (ESG) criteria is influencing banking regulation, risk assessment, and financing decisions. The CBI and international institutions are promoting ESG integration to improve governance, transparency, and sustainable financing practices within the financial sector. Banks that adopt ESG frameworks strengthen credibility with investors, lenders, and regulators. ESG components applied in bank: Environmental: energy use, emissions, climate risks Social: customer protection, labor practices, financial inclusion Governance: board oversight, compliance, transparency CBI and supervisory expectations may include: ESG reporting standards Integration of ESG into risk management Disclosure of sustainability metrics How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Mergers of Exchange Companies in Iraq

Mergers of Exchange Companies in Iraq Mergers between FX companies are subject to regulatory oversight due to the impact on market concentration, ownership transparency, and compliance standards. Mergers may be pursued for scale, capital consolidation, geographic expansion, or to meet regulatory requirements for higher categories. No merger can proceed without prior CBI approval to ensure suitability of the resulting entity. Procedures generally required in mergers: Submission of merger request to CBI Due diligence on both entities Assessment of ownership and management structure Capital adequacy and financial consolidation Amendments to corporate documents and licenses Final regulatory approval and registration Documentation typically required: Corporate merger agreements Shareholder resolutions Financial statements and asset valuations Proposed post-merger ownership chart Source of funds documentation AML/CFT compliance reports Capital and branch structure reports CBI compliance expectations Meet the required capital thresholds Maintain a compliant ownership structure Retain qualified senior management Update AML/CFT frameworks and reporting How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Renewable Energy Initiative Guidelines

Renewable Energy Initiative Guidelines Renewable energy initiatives are gaining support in Iraq as part of diversification and energy transition goals. Financial institutions are expected to develop products and risk assessment models suitable for financing renewable projects such as solar, wind, and hybrid energy systems. CBI encourages lending that supports sustainable development and long-term economic stability. Practical implications for banks: Development of renewable financing products Technical and project risk assessment capabilities Coordination with government programs or incentives Integration of ESG elements into financing decisions Regulatory considerations Allocate credit to priority sectors Conduct due diligence on project viability Monitor repayment capacity tied to power offtake agreements Align with environmental disclosure practices How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Shareholder Structure Requirements in Banks

Shareholder Structure Requirements in Banks Bank shareholders, especially those holding significant ownership stakes, are subject to supervisory oversight due to their influence on strategic decisions and capital soundness. Ownership of banks in Iraq may be held by individuals, companies, or foreign institutions, but all must comply with ownership thresholds, transparency requirements, and regulatory approvals for significant share acquisitions. Share transfers or new entries of major shareholders often require prior CBI review to prevent improper influence or financial instability. Transactions that typically trigger regulatory review: Acquisition of significant shareholding percentages Transfer of ownership stakes Changes in controlling shareholders Foreign shareholder entry Capital increases or capital restructuring Documentation typically required: Shareholder identification and corporate documents Source of funds disclosure Financial statements or net worth statements Business profile of corporate shareholders Declarations regarding legal standing Board/Shareholder resolutions CBI compliance expectations Maintain transparent shareholding records Obtain CBI approval for qualifying holdings Ensure shareholder financial soundness Prevent non-approved control or influence Comply with capital adequacy requirements linked to ownership How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

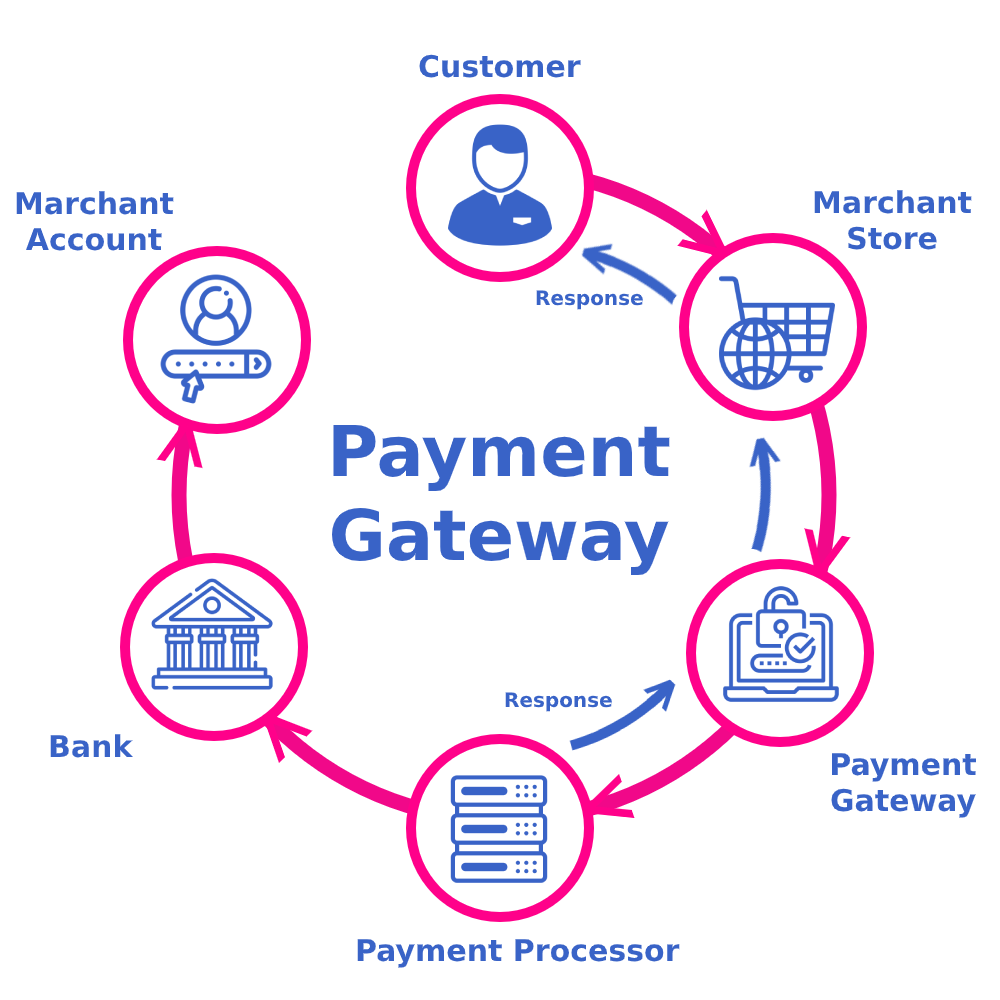

AML & KYC Obligations for Electronic Payment Providers

AML & KYC Obligations for Electronic Payment Providers Electronic Payment Service Providers (EPSPs) handle transactions that can be exposed to money laundering, terrorist financing, fraud, and sanctions risks. For this reason, CBI imposes mandatory Anti-Money Laundering (AML) and Know-Your-Customer (KYC) obligations on EPSPs similar to those applied to banks, with additional expectations for digital onboarding and transaction monitoring. Compliance is essential for maintaining regulatory approval and protecting the digital payment ecosystem. AML/KYC Requirements Customer identification and verification procedures Enhanced Due Diligence (EDD) for high-risk users Continuous monitoring of transactions and behavior Sanctions and PEP list screening Suspicious transaction reporting Record-keeping and audit trails Operational Requirements for Digital KYC Secure digital onboarding channels Document verification tools or manual controls Data retention and privacy protections CBI compliance Maintain written AML/KYC policies and manuals Establish an AML Compliance Officer and team Integrate technology for real-time monitoring Report suspicious activities in prescribed formats Submit periodic AML compliance reports Cooperate with supervisory inspections How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Establish a Bank in Iraq

Establish a Bank in Iraq Establishing a bank in Iraq involves a structured licensing process supervised by the Central Bank of Iraq. Investors must demonstrate financial capacity, provide a viable business model, and establish governance, risk, and compliance frameworks before receiving authorization. Banking establishment may be pursued through incorporation of a new entity or via entry as a foreign branch or subsidiary. The process is multi-stage and requires alignment with regulatory, capital, ownership, and AML standards before commencing operations. Steps in the establishment process: Submission of initial application and feasibility/business plan Review of ownership structure and capital sources Fit & proper assessment of controllers and management Approval of governance and risk management frameworks Issuance of preliminary and final CBI authorizations Registration with relevant Iraqi authorities Documentation required from investors: Corporate registration and identification documents Business plan and financial projections Capital and source-of-funds evidence Shareholder disclosures Proposed Board & senior management profiles Risk, audit, and compliance documentation AML/KYC policies CBI compliance expectations Satisfy minimum capital requirements Meet ownership suitability standards Establish risk, audit, and compliance functions Implement AML/CFT systems Maintain reporting and prudential ratios Appoint approved Board and senior management Obtain full authorization before commercial activity How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Digital Banking Transformation and Regulatory Readiness in Iraq – Copy

Credit Facilities and Collateralization Practices in Iraq Credit facilities are a core component of corporate banking in Iraq, with lending typically supported by collateral to mitigate credit risk. Collateral may include real estate, equipment, receivables, inventory, shares, and personal or corporate guarantees. Key Concepts in Credit Transactions Structuring bilateral and syndicated loans Collateral valuation and security perfection Registration of security interests Enforcement of guarantees and mortgages Priority of security rights Insolvency implications Common Security Instruments Registered mortgages Pledges over movable assets and shares Assignment of receivables Letters of guarantee Personal guarantees How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Cybersecurity & Incident Reporting Requirements

Cybersecurity & Incident Reporting Requirements Cybersecurity is a core regulatory concern for electronic payment operations due to the sensitivity of financial data and the systemic impact of cyber incidents. EPSPs must protect platforms, user data, and transaction networks against breaches, fraud, hacks, and unauthorized access. Regulators also require timely incident reporting to limit supervisory and market risks. Cybersecurity Controls Firewalls and intrusion prevention systems Encryption of sensitive data Access controls and multi-factor authentication Incident Reporting Requirements Timely notification to the CBI for material incidents Documentation of breach details and impact Implementation of corrective actions and mitigation steps CBI compliance Maintain cybersecurity policies and frameworks Conduct periodic risk assessments Monitor systems for anomalies and threats Implement incident reporting and escalation procedures How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.

Senior Leadership Appointments in Banks

Senior Leadership Appointments in Banks Appointments to senior leadership positions in Iraqi banks require regulatory clearance due to the impact these roles have on governance, risk oversight, and compliance. Positions such as Board Members, CEO, CFO, Chief Risk Officer, and Compliance/AML Officers are subject to CBI review to ensure competence, integrity, and suitability (“fit and proper”) of appointees. The process aims to strengthen governance and reduce financial stability risks. In practice, banks cannot finalize key appointments without CBI approval, making planning and documentation essential for regulatory compliance. Positions typically requiring CBI approval Board of Directors (Executive & Non-Executive) Chief Executive Officer (CEO / GM) Chief Financial Officer (CFO) Head of Internal Audit Head of Risk Management Compliance & AML Officers Senior Management with control functions Documentation typically required: Curriculum Vitae and qualifications Professional certificates (if applicable) No-criminal-record certificates Experience statements Declaration of financial soundness Conflict of interest declarations Identification and corporate approvals CBI compliance expectations Conduct internal fit & proper checks Ensure adequate experience in banking/finance Verify integrity and financial standing Submit documents for regulatory review Notify CBI of changes in leadership roles Maintain governance structures aligned with supervisory expectations How Etihad Can Assist Etihad provides legal and regulatory advisory services to banks, financial institutions, and businesses, supporting compliance with applicable laws, regulations, and regulatory guidance issued by any competent authorities.