LC Disputes in Iraq: Courts or Arbitration?

LC Disputes in Iraq: Courts or Arbitration? When a letter of credit transaction goes wrong whether through wrongful rejection of documents, non-payment by the issuing bank, or allegations of fraud the parties face an immediate question: where and how to resolve the dispute? In Iraq, as in other markets, the choice between pursuing claims before Iraqi courts and submitting to international arbitration has significant practical implications for the speed, cost, and likely outcome of dispute resolution. This article examines the options available for resolving LC disputes involving Iraqi parties, the relative merits of each, and the key considerations that should inform the choice of forum. The Nature of LC Disputes LC disputes arise in a variety of circumstances, including: wrongful rejection, the issuing or confirming bank refuses to pay despite the presentation of compliant documents; wrongful dishonour the bank fails to pay on time or refuses on grounds not supported by UCP 600; discrepancy disputes, parties disagree on whether specific documents are compliant; fraud disputes, one party alleges that documents are forged or that the presentation is fraudulent; and underlying contract disputes, the buyer claims the goods are defective or do not conform to the commercial contract. Each type of dispute has different characteristics that affect the appropriate forum choice. Iraqi Courts — Jurisdiction and Practice Iraqi courts have jurisdiction over LC disputes where: the issuing bank is licensed in Iraq; the LC transaction was performed in Iraq; or the parties have agreed to Iraqi court jurisdiction. Commercial disputes in Iraq are heard by the commercial courts specialised divisions of the civil courts with experience in commercial matters. Iraqi courts apply Iraqi law as the applicable substantive law for disputes before them, supplemented by UCP 600 provisions incorporated into the LC. Key practical considerations for Iraqi court proceedings include: proceedings are conducted in Arabic, foreign parties need qualified translators and Iraqi legal representation; the timeline for commercial court proceedings varies significantly; and enforcement of an Iraqi court judgment against a foreign party requires separate proceedings in the foreign jurisdiction. International Arbitration — ICC, LCIA, and DIFC-LCIA International arbitration is increasingly used to resolve trade finance disputes involving Iraqi parties, particularly where one or more parties are foreign. The most commonly used arbitral institutions for Iraq-related disputes include: International Chamber of Commerce (ICC), the most widely used institution for international commercial arbitration globally, with well-established procedures and a strong track record of enforcing awards; London Court of International Arbitration (LCIA) widely used for disputes involving English law-governed documents; and DIFC-LCIA, the arbitration centre in the Dubai International Financial Centre, increasingly popular for Middle East disputes due to its geographic proximity and the enforceability of its awards in the region. Iraq and the New York Convention Iraq acceded to the New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards in 2008. This means that arbitral awards rendered in signatory states can be enforced in Iraq through the Iraqi courts, subject to the limited grounds for refusal specified in the Convention. In practice, enforcement of New York Convention awards in Iraq has worked, though the process requires filing an enforcement application with the competent Iraqi court. The availability of New York Convention enforcement is a significant advantage of international arbitration over foreign court judgments for parties dealing with Iraqi counterparties. Choosing the Right Forum — Key Considerations The choice between Iraqi courts and international arbitration for LC disputes should consider: the nature of the dispute straightforward document rejection disputes may be suitable for Iraqi courts; complex, high-value disputes benefit from international arbitration’s procedural sophistication; the nationality of the parties foreign parties typically prefer international arbitration to avoid perceived home court advantages; the governing law English law-governed LCs are better suited to English-seat arbitration or London courts; speed and cost Iraqi courts may offer faster resolution for straightforward matters, while arbitration provides more predictable procedures for complex disputes; and enforcement needs where the award must be enforced against assets in multiple jurisdictions, international arbitration with New York Convention enforcement provides the broadest reach. Drafting Effective Dispute Resolution Clauses Effective dispute resolution clauses in LC-related documents including the underlying commercial contract and any security documents should: specify the chosen arbitral institution and procedural rules clearly; designate the seat of arbitration; specify the number of arbitrators and selection mechanism; specify the governing law; address urgent interim relief specifying whether parties may seek emergency arbitrator relief or must go to national courts; and address confidentiality of proceedings. Ambiguous or poorly drafted dispute resolution clauses create jurisdictional disputes before the substantive dispute is even addressed. How Etihad Law Firm Assists Etihad represents clients in LC disputes before Iraqi commercial courts and in international arbitration proceedings. We advise on forum selection, draft effective dispute resolution clauses in trade finance documents, manage Iraqi court enforcement proceedings for foreign arbitral awards, and provide urgent advisory services when LC disputes arise.

Trade Finance Fraud in Iraq

Trade Finance Fraud in Iraq Trade finance fraud is a global problem, and Iraq as a major import market with a complex regulatory environment is not immune. From forged shipping documents and fictitious invoices to phantom shipments and duplicate financing fraud, the range of schemes targeting trade finance transactions is broad and constantly evolving. For Iraqi banks, importers, and their legal advisers, understanding the types of fraud that occur in the trade finance context, the legal remedies available under Iraqi law and international trade finance rules, and the prevention strategies that reduce vulnerability is essential. Common Forms of Trade Finance Fraud in Iraq The most common forms of trade finance fraud affecting Iraqi transactions include: document fraud — forging or altering shipping documents, invoices, certificates of origin, or inspection certificates to present a compliant presentation under an LC when the actual goods do not conform to LC terms or do not exist; phantom shipment presenting documents for goods that were never shipped, typically involving forged bills of lading; over-invoicing presenting inflated invoices to obtain LC payment exceeding the actual value of goods, often used to disguise capital flight; duplicate financing using the same goods or shipping documents to obtain financing from multiple banks simultaneously; and manipulation of inspection certificates bribing inspection agency personnel to certify non-conforming goods as compliant. The Fraud Exception Under UCP 600 UCP 600 is built on the principle of documentary independence banks pay against documents, not against the underlying transaction. However, all legal systems recognise a fraud exception: where the presentation of documents is clearly fraudulent meaning the beneficiary knows the documents are forged or that it has no legitimate claim, a court may restrain the bank from paying. The fraud exception under UCP 600 is narrow: it requires clear, established fraud, not merely allegations or suspicion. A disputed commercial transaction where the goods are delivered but the importer claims they are substandard does not constitute fraud for LC purposes. Iraqi Legal Remedies for Trade Finance Fraud Iraqi law provides several remedies for victims of trade finance fraud. Under the Iraqi Penal Code, forgery of commercial documents is a criminal offence punishable by imprisonment. Iraqi banks and companies that discover document fraud should file criminal complaints with the competent Iraqi investigative authorities. Civil remedies include: claims for damages against the fraudulent party; injunctive relief to restrain LC payment where fraud is established; and recovery of funds paid under fraudulently obtained LCs through civil court proceedings. Iraqi courts have jurisdiction over fraud claims where: the fraud was committed in Iraq; the fraudulent party is located in Iraq; or the bank that made payment is licensed in Iraq. Injunctions to Restrain LC Payment — Iraqi Court Practice Where an Iraqi bank or importer discovers document fraud before payment is made under an LC, an urgent injunction application may be filed with the competent Iraqi court to restrain payment. Iraqi courts may grant interim injunctions restraining bank payment where there is credible evidence of fraud and the balance of convenience favours restraint. The applicant must act immediately, once the bank has paid, injunctive relief is academic. The applicant must provide the court with clear documentary evidence of fraud, not merely allegations based on commercial suspicion. Iraqi courts’ approach to LC injunctions is developing, and the outcome of applications depends significantly on the strength of evidence and the competence of legal representation. AML Implications of Trade Finance Fraud Trade finance fraud frequently intersects with AML violations. Over-invoicing, phantom shipments, and duplicate financing are used not only for direct financial gain but also as mechanisms for money laundering moving illicit funds across borders disguised as legitimate trade transactions. Iraqi banks are required under AML Law No. 39 of 2015 and CBI AML instructions to implement trade finance-specific AML controls, including: transaction monitoring for unusual LC patterns; enhanced due diligence on high-risk counterparties and jurisdictions; verification of the economic rationale of trade transactions; and cross-referencing of LC documentation against independent commercial databases. Prevention Strategies for Iraqi Banks and Traders Prevention of trade finance fraud requires a multi-layered approach: banks should implement pre-shipment inspection requirements for high-risk transactions and goods; independent verification of shipping documents through reputable inspection agencies; automated duplicate financing detection systems; enhanced due diligence on first-time customers and unfamiliar counterparties; staff training on document fraud detection; and information sharing with other banks and the CBI on identified fraud patterns. Traders should conduct thorough due diligence on their counterparties, use reputable freight forwarders, and consider using confirmed LCs where the issuing bank’s document examination quality is uncertain. How Etihad Law Firm Assists Etihad advises Iraqi banks and companies on legal remedies for trade finance fraud, including urgent injunction applications, criminal complaints, and civil recovery proceedings. We also advise on AML compliance frameworks for trade finance and on due diligence procedures to reduce fraud vulnerability.

Standby Letters of Credit vs Bank Guarantees

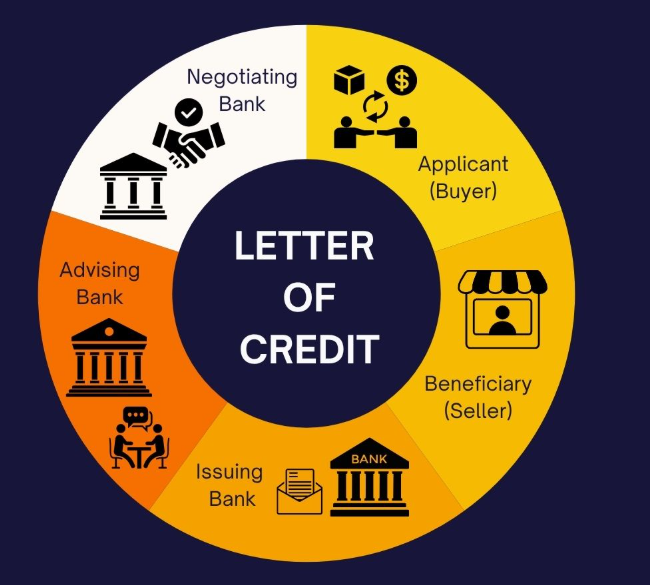

Standby Letters of Credit vs Bank Guarantees Standby letters of credit and bank guarantees are both widely used security instruments in commercial transactions, and they share a common economic function: providing a beneficiary with an independent bank undertaking to pay in the event of the principal’s default. Yet the two instruments have distinct legal frameworks, different governing rules, and important practical differences that affect their suitability for specific transactions in Iraq. Understanding when to use a standby LC versus a bank guarantee and how each is regulated in Iraq is essential knowledge for banks, corporate clients, and legal advisers. The Fundamental Distinction A standby letter of credit is a letter of credit that functions as a guarantee, it is intended to be drawn upon only if the applicant fails to perform its underlying obligation. Like a commercial LC, it is governed by UCP 600 (or ISP98) and involves a bank’s undertaking to pay against compliant documents. A bank guarantee is a separate instrument an independent undertaking by a guarantor bank to pay upon a compliant demand, governed by URDG 758 or applicable national law. While both instruments achieve similar security objectives, their legal framework, documentation, and demand mechanics differ significantly. ISP98 — The Rules for Standby LCs The International Standby Practices (ISP98) is a set of rules published by the ICC specifically designed for standby letters of credit. ISP98 provides more detailed and appropriate rules for standbys than UCP 600, which was primarily designed for commercial (documentary) LCs. Key ISP98 features include: detailed rules on the types of documents that may be required under a standby; specific provisions for automatic extension and non-extension of standbys; and rules on transfer and assignment of standby proceeds. Standby LCs can be issued subject to ISP98 (preferred for standbys) or UCP 600. In Iraq, many standby LCs are issued subject to UCP 600 due to greater bank familiarity, but ISP98 provides a more appropriate framework. Bank Guarantees Under URDG 758 in Iraq Bank guarantees issued by Iraqi banks are typically subject to URDG 758, which provides the internationally recognised framework for demand guarantees. Iraqi banks issuing guarantees for construction contracts, public tenders, and other commercial purposes commonly incorporate URDG 758. CBI instructions on guarantee issuance require Iraqi banks to document guarantee transactions carefully and maintain adequate records. The key advantage of URDG 758 over UCP 600 for guarantee transactions is that URDG 758 is purpose-built for demand guarantees its provisions more precisely address the dynamics of guarantee calls, counter-guarantees, and extend-or-pay demands. CBI Treatment of Standby LCs and Guarantees The CBI regulates both standby LCs and bank guarantees issued by Iraqi licensed banks. Key CBI requirements include: capital treatment, guarantees and standby LCs are treated as contingent liabilities for capital adequacy purposes under the CBI’s Basel III implementation; exposure limits the total guarantee and standby LC exposure to a single counterparty is subject to the CBI’s single counterparty exposure limits; documentation requirements, banks must maintain complete documentation for all guarantees and standby LCs issued; and reporting requirements, banks must report their guarantee and standby LC portfolios to the CBI as part of periodic prudential reporting. When to Use a Standby LC vs a Bank Guarantee in Iraq The choice between a standby LC and a bank guarantee in Iraqi transactions depends on several factors: jurisdiction and acceptability, some Iraqi government entities and project owners specify which instrument they require, and their requirements should be followed; governing rules preference, parties who prefer URDG 758 governance should use a bank guarantee; demand mechanics, URDG 758’s supporting statement requirement provides slightly more protection for principals than a standard standby LC demand; international transactions for transactions involving US or Latin American counterparties, standby LCs are more commonly used and more familiar to those parties; and construction and infrastructure in Iraq, bank guarantees under URDG 758 are the standard instrument for FIDIC-based construction contracts. Tax and Accounting Treatment The tax and accounting treatment of standby LCs and bank guarantees in Iraq may differ. Banks must account for guarantees and standby LCs as contingent liabilities on their balance sheets. The fee income received from issuing these instruments is treated as non-interest income. For corporate clients, guarantee fees paid are generally deductible business expenses, but the tax treatment of specific structures should be confirmed with Iraqi tax advisers. IFRS 9 and IFRS 4 contain specific accounting requirements for financial guarantee contracts that must be applied by Iraqi IFRS-reporting entities. How Etihad Law Firm Assists Etihad advises clients on the selection, structuring, and documentation of standby LCs and bank guarantees for Iraqi transactions, reviews instrument terms for compliance with UCP 600, ISP98, and URDG 758, and advises on disputes arising from calls on these instruments.

Import Letters of Credit in Iraq

Import Letters of Credit in Iraq Iraq is one of the largest import markets in the Middle East, with a diverse range of goods from food and medicine to construction materials and electronics imported through documentary credits. For Iraqi companies importing goods, opening a letter of credit involves navigating not just UCP 600 requirements but also a specific regulatory process involving the CBI’s foreign currency allocation system, Ministry of Trade approvals for certain goods, and Iraqi customs documentation requirements. This article provides a comprehensive guide to the import LC process in Iraq, from initial commercial contract to final payment and goods clearance. Why LCs Dominate Iraqi Import Finance Letters of credit dominate Iraqi import finance for a combination of commercial and regulatory reasons. From the foreign exporter’s perspective, an LC provides a bank payment undertaking, eliminating reliance on the Iraqi importer’s creditworthiness and providing security of payment. From the Iraqi importer’s perspective, the LC provides assurance that payment will only be made against documents evidencing that the goods have been shipped as agreed. From a regulatory perspective, the CBI’s foreign currency system is structured around LCs, importers access USD for import payments primarily through the LC mechanism, which allows the CBI to monitor and control foreign currency outflows. Step 1 — Commercial Contract and LC Terms Agreement The import LC process begins with the commercial contract between the Iraqi importer and the foreign exporter. The contract should specify: that payment is by irrevocable LC subject to UCP 600; the LC amount, currency, and any tolerance; the documents required for payment typically commercial invoice, bill of lading, packing list, certificate of origin, and any Iraq-specific documents; the latest shipment date and LC expiry date; the port of shipment and destination; and any special conditions such as inspection requirements. Poorly drafted LC terms at this stage are the primary source of subsequent discrepancy disputes. Step 2 — CBI Foreign Currency Application Before an Iraqi bank can issue an import LC, it must obtain USD allocation through the CBI’s foreign currency auction system. The importer’s bank applies to the CBI for foreign currency on behalf of the importer, providing: details of the import transaction including the pro-forma invoice; documentation confirming the legitimacy of the import; and AML/KYC documentation on the importer and the foreign exporter. The CBI reviews applications and allocates foreign currency based on available reserves, the nature of the goods, and compliance with CBI criteria. Goods on the CBI’s restricted or prohibited list may not obtain foreign currency allocation. This step is unique to the Iraqi LC market and has no equivalent in most other jurisdictions. Step 3 — Ministry of Trade and Other Government Approvals Certain categories of imported goods require Ministry of Trade approval before an LC can be opened. Goods requiring Ministry of Trade approval include certain food products, consumer goods, and goods subject to quality or safety standards. For medical and pharmaceutical imports, Ministry of Health approval is required. For goods with national security implications, approval from relevant security authorities may be required. The importer must obtain these approvals before the bank submits its CBI currency application, as the approvals are typically required documentation for the currency allocation request. Step 4 — LC Application and Bank Credit Approval Once foreign currency is allocated, the importer submits a formal LC application to its bank. The bank’s trade finance department reviews the application and if the importer does not have a pre-approved trade finance facility, the credit department assesses the importer’s creditworthiness and approves the LC issuance. The bank determines the cash coverage requirement, the percentage of the LC amount the importer must deposit or have available as security before the LC is issued. Cash coverage requirements vary by bank and by the importer’s credit standing, typically ranging from 20% to 100% of the LC amount. Step 5 — LC Issuance and Transmission Upon credit approval and receipt of cash coverage, the Iraqi bank issues the LC through the SWIFT messaging system, transmitting it to the advising bank in the exporter’s country. The LC message specifies all terms and conditions, documents required, latest shipment date, expiry date, and any special conditions. The advising bank authenticates the LC and advises it to the exporter, confirming the LC’s authenticity and terms. If the exporter requires a confirmed LC, the advising bank adds its confirmation at this stage, subject to the exporter’s bank’s credit assessment of the Iraqi issuing bank. How Etihad Law Firm Assists Etihad advises Iraqi importers on the full import LC process, from negotiating LC terms in commercial contracts to resolving disputes with banks or foreign exporters. We advise on CBI requirements, Ministry of Trade approvals, document compliance, and represent clients in import LC disputes.

Documentary Discrepancies in Iraqi Trade Finance

UCP 600 and Iraqi Banking Practice The Uniform Customs and Practice for Documentary Credits (UCP 600) is the international standard governing letters of credit in virtually all trading jurisdictions and Iraq is no exception. Iraqi banks incorporate UCP 600 into their LC transactions by reference, subjecting the transaction to its 39 articles. However, the interaction between UCP 600 and Iraq-specific regulatory requirements, CBI instructions, and local banking practice creates a landscape where international standard and local reality do not always align perfectly. Understanding these alignments and divergences is essential for traders, banks, and legal advisers involved in Iraqi LC transactions. Where Iraqi Practice Aligns with UCP 600 In core documentary credit principles, Iraqi banking practice generally aligns with UCP 600: the principle of documentary independence, Iraqi banks treat the LC as independent of the underlying commercial contract, examining documents on their face without reference to the goods or the commercial relationship; the five banking day examination period, Iraqi banks are expected to examine documents and give notice of acceptance or refusal within five banking days; the strict compliance standard Iraqi banks apply the strict compliance standard in examining documents, rejecting presentations that deviate from LC terms; and the preclusion rule, banks that fail to give timely notice of refusal are precluded from later claiming discrepancies. Where CBI Requirements Add to UCP 600 CBI instructions create additional requirements on top of UCP 600 that affect LC practice in Iraq. These include: mandatory goods inspection requirements for certain categories of imported goods, the CBI requires inspection by approved inspection agencies before LC payment, adding a document requirement beyond the standard UCP 600 framework; certificate of origin requirements, Iraqi customs authorities require certificates of origin for most imported goods, and CBI instructions require these to be included in LC document requirements; Ministry of Trade approvals certain categories of goods require Ministry of Trade import approvals that must be obtained before LC issuance, creating a pre-condition not addressed by UCP 600; and AML documentation, CBI AML requirements mandate due diligence on LC applicants and beneficiaries that goes beyond the documentary focus of UCP 600. Practical Divergences in Iraqi LC Practice Practical divergences between UCP 600 standards and Iraqi banking practice include: document examination quality, the standard of UCP 600-compliant document examination varies among Iraqi banks, with some institutions applying less rigorous standards than ISBP 821 requires, creating uncertainty for presenters; communication timelines while UCP 600 requires notice of refusal within five banking days, communication delays can occur in practice due to staffing and operational factors; amendment processing amendments to Iraqi LCs may take longer to process than UCP 600 timelines anticipate, due to internal approval requirements; and electronic documentation, Iraqi banks are at varying stages of readiness for electronic document presentations under eUCP. The Autonomy Principle in Iraqi Courts The autonomy principle that the LC is independent of the underlying commercial contract is recognised under Iraqi law. However, Iraqi courts’ approach to LC injunction applications differs from common law jurisdictions. In common law systems, courts apply the fraud exception narrowly, granting injunctions only in clear cases of established fraud. Iraqi courts applying civil law principles may take a broader approach to intervening in LC transactions, creating a risk for beneficiaries that payment may be restrained on grounds that would not satisfy the fraud exception under UCP 600 and international banking practice. This difference is an important risk factor for beneficiaries under Iraqi-issued LCs. ISBP 821 — International Standard Banking Practice in Iraq ISBP 821 provides detailed guidance on how specific documents should be examined under UCP 600. Awareness and application of ISBP 821 among Iraqi banks varies. Exporters should be aware that document preparation standards meeting ISBP 821 requirements which are the internationally recognised standard may not always be interpreted consistently by Iraqi issuing banks. This creates a risk of discrepancy notices based on standards that differ from international practice. Presenting documents through a confirmed LC where the confirming bank applies consistent ISBP 821 standards mitigates this risk. Risk Management Strategies for Iraqi LC Transactions Parties to Iraqi LC transactions should adopt the following risk management strategies: exporters should always request a confirmed LC where possible eliminating dependence on the Iraqi issuing bank’s document examination practice; parties should negotiate clear, unambiguous LC terms that reduce the risk of discrepancy; exporters should present documents through experienced trade finance banks familiar with Iraqi banking practice; and legal counsel should be engaged to review complex LC terms and advise on UCP 600 compliance before shipment. How Etihad Law Firm Assists Etihad advises traders, banks, and corporate clients on the interaction between UCP 600 and Iraqi banking practice, reviewing LC terms for compliance risks, advising on document preparation to minimise discrepancy risk, and representing clients in LC disputes before Iraqi courts and arbitral tribunals.

UCP 600 and Iraqi Banking Practice

Documentary Discrepancies in Iraqi Trade Finance Documentary discrepancies failures of presented documents to comply with letter of credit terms are the single most common cause of payment delays and disputes in trade finance globally. In Iraqi trade finance, the challenge is compounded by the interaction of UCP 600 examination standards with Iraq-specific documentation requirements imposed by CBI instructions, Ministry of Trade regulations, and customs authorities. For Iraqi importers, exporters, and the banks that serve them, understanding and managing the risk of documentary discrepancies is a commercial priority. This article provides a comprehensive guide to documentary discrepancies in the Iraqi trade finance context. The Scale of the Problem International Chamber of Commerce research consistently shows that 60-70% of first presentations under letters of credit globally contain at least one discrepancy. In Iraq-related LC transactions, the discrepancy rate may be higher due to: the complexity of Iraq-specific documentation requirements imposed by CBI instructions and customs regulations; the involvement of multiple government approvals in certain import categories; language and translation requirements for Arabic documentation; and the quality of document preparation by exporters unfamiliar with Iraqi-specific requirements. A single discrepancy however minor can delay payment by days or weeks while waiver is sought, creating cash flow difficulties for exporters and supply chain disruptions for importers. Iraq-Specific Documentation Requirements Beyond standard UCP 600 document requirements, Iraqi LCs typically include Iraq-specific documents that create additional discrepancy risk: certificate of origin must be issued by the competent authority in the country of origin in the form required by Iraqi customs; inspection certificate for regulated goods, a certificate from an approved inspection agency (such as SGS or Bureau Veritas) confirming goods conform to specifications; import licence or Ministry of Trade approval where required for the specific goods category; packing list must contain detailed information matching the invoice and bill of lading; and health or phytosanitary certificates for food, agricultural, and pharmaceutical imports. Each of these documents must comply exactly with the LC terms any deviation in format, content, or authentication constitutes a discrepancy. The Five Most Common Discrepancies in Iraqi Trade Finance Based on Iraqi trade finance practice, the five most frequent discrepancies are: late presentation documents presented after the LC’s expiry date or beyond the presentation period (typically 21 days from the bill of lading date, unless the LC specifies otherwise); late shipment, the bill of lading or other transport document is dated after the latest shipment date specified in the LC; description of goods the description of goods in the commercial invoice does not match the LC; certificate of origin deficiencies the certificate is not from the required authority, is not properly authenticated, or does not describe the goods as required; and inconsistencies between documents, the country of origin, goods description, quantity, or other details differ between the invoice, packing list, certificate of origin, and bill of lading. The Examination Process Under Iraqi Bank Practice Iraqi banks examining documents presented under LCs they have issued are required to apply the UCP 600 examination standard examining documents on their face within five banking days of presentation. In practice, the examination process at Iraqi banks involves: initial review by the trade finance department; assessment of compliance with both UCP 600 requirements and CBI-specific documentation requirements; review of any Iraqi customs documentation requirements; and escalation to senior management for significant discrepancies or waiver decisions. Banks that are uncertain about document compliance may seek guidance from their correspondent banks or from the ICC. The Waiver Process in Iraqi Practice When documents are found to be discrepant, the Iraqi issuing bank typically contacts the applicant (importer) to seek a waiver. The importer reviews the discrepancies and decides whether to waive accepting the goods and documents despite the discrepancies or reject. In Iraqi practice, waiver decisions are often commercially driven: where the importer is satisfied with the goods and has a continuing relationship with the exporter, waiver is common. Where the importer has a commercial reason to reject such as a fall in commodity prices making the goods less attractive, discrepancies may be used as a basis for rejection. Exporters should be aware that discrepant presentations give importers leverage that they may use commercially. Preventing Discrepancies — Practical Steps for Iraqi Trade Exporters dealing with Iraqi importers should: review the LC immediately upon receipt before making any shipping arrangements; identify all document requirements including Iraq-specific requirements; request LC amendments before shipment if any terms cannot be met; prepare a checklist of all required documents against the LC terms; ensure all documents are consistent with each other, not just with the LC; use experienced freight forwarders and shipping agents familiar with Iraqi trade documentation; present documents promptly do not wait until the expiry date; and where significant value is involved, have documents reviewed by trade finance legal counsel before presentation. How Etihad Law Firm Assists Etihad advises exporters and importers on documentary compliance in Iraqi trade finance, reviews LC terms before shipment to identify discrepancy risks, advises on the waiver process and negotiation of discrepancy disputes, and represents clients in legal proceedings arising from wrongful rejection of compliant documents or improper handling of discrepant presentations.

Restructuring Distressed Loans in Iraq

Restructuring Distressed Loans in Iraq Loan restructuring renegotiating the terms of a loan that the borrower is struggling or unable to service is an increasingly important area of Iraqi banking practice. Non-performing loans (NPLs) represent a significant challenge for Iraqi banks, reflecting both the legacy of past economic disruptions and the ongoing challenges of the credit environment. For borrowers in financial difficulty, and for lenders seeking to maximise recovery on distressed exposures, understanding the legal options for loan restructuring in Iraq is essential. This article examines the CBI’s NPL framework, available restructuring mechanisms, and how international best practice applies in the Iraqi context. CBI Non-Performing Loan Classification The CBI requires Iraqi banks to classify their loan portfolios according to asset quality categories: performing loans where principal and interest payments are current and the borrower’s financial condition is sound; watch loans where the borrower is experiencing minor financial difficulties but remains current on payments; substandard loans where repayment is in doubt and the borrower is more than 90 days past due; doubtful loans where full repayment is unlikely and the borrower is more than 180 days past due; and loss loans that are considered uncollectable and more than 360 days past due. Each category requires specific provisioning levels, with loss loans requiring 100% provisioning. The CBI monitors banks’ NPL ratios and provisioning levels as part of its supervisory function. Out-of-Court Restructuring Options The most common approach to distressed loan restructuring in Iraq as in most markets is an out-of-court negotiated restructuring between the bank and the borrower. Out-of-court restructuring options include: rescheduling extending the loan maturity and adjusting the repayment schedule to reflect the borrower’s current cash flow capacity; interest rate reduction reducing the applicable interest rate to ease the borrower’s debt service burden; grace period granting a moratorium on principal repayments for a specified period while the borrower stabilises its financial position; debt-to-equity conversion converting part of the outstanding loan into equity in the borrower, giving the bank a shareholding in the business; partial debt forgiveness writing off a portion of the outstanding debt in exchange for improved security or other consideration; and additional security the borrower provides additional collateral to enhance the bank’s recovery prospects. Iraqi Bankruptcy Law Iraq does not currently have a modern, comprehensive insolvency law equivalent to those in developed markets. The applicable legal framework for insolvency of commercial entities is primarily found in the Iraqi Commercial Law No. 30 of 1984, which contains provisions on bankruptcy (iflas) and composition (sulh). The Iraqi bankruptcy framework is court-supervised and creditor-initiated, a creditor may file for a debtor’s bankruptcy where the debtor has ceased payment of its commercial debts. The court appoints a trustee to manage the bankrupt estate and distribute assets to creditors. Reform of Iraqi insolvency law is a long-recognised need, and legislative reform proposals have been under consideration for a number of years. CBI Requirements for Loan Restructuring The CBI has issued instructions on the restructuring of non-performing loans by Iraqi banks. Key requirements include: restructuring agreements must be approved by the bank’s credit committee and board of directors in accordance with the bank’s credit policy; restructured loans must be classified and provisioned in accordance with CBI classification instructions reclassification to a better category is subject to specified conditions and observation periods; any forgiveness of debt or reduction in interest must be accounted for in accordance with IFRS 9 requirements; and banks must report restructured loans to the CBI as part of their periodic prudential reporting. CBI approval may be required for restructurings of significant exposures or restructurings involving related parties. International Best Practice — The London Approach The London Approach a set of informal principles developed by the Bank of England for multi-creditor workouts has become a reference point for restructuring practice internationally. While not legally binding in Iraq, its core principles are increasingly applied in complex Iraqi restructurings involving multiple creditors: standstill creditors agree to refrain from enforcement action while restructuring negotiations proceed; information sharing the borrower provides full financial information to all creditors; equal treatment no creditor should receive preferential treatment; and negotiation in good faith all parties commit to reaching a consensual resolution. Intercreditor agreements coordinating the positions of multiple bank creditors are an important tool in multi-creditor Iraqi restructurings. Practical Considerations for Lenders Lenders considering restructuring distressed Iraqi loans should: assess security validity and enforceability before agreeing to restructuring understanding the practical enforceability of existing security is essential to evaluating the restructuring alternative; obtain independent financial advice on the borrower’s viability restructuring is only appropriate where the business has long-term viability; document all restructuring steps carefully restructuring agreements must be formally documented to be enforceable; consider tax implications of debt forgiveness debt forgiveness may have tax consequences for both the borrower and the lender under Iraqi tax law; and engage early the earlier a lender engages with a distressed borrower, the more restructuring options are available. How Etihad Law Firm Assists Etihad advises lenders and borrowers on distressed loan restructurings in Iraq. We assist in negotiating and documenting restructuring agreements, advise on CBI requirements for loan reclassification following restructuring, represent clients in formal insolvency proceedings under Iraqi commercial law, and advise on security enforcement as an alternative to restructuring where appropriate.

Legal Structure and Lender Requirements

Legal Structure and Lender Requirements Project finance where debt is repaid from the cash flows generated by a specific project rather than from the general assets of a sponsor is the financing model of choice for major infrastructure, energy, and industrial projects in Iraq. The country’s significant infrastructure deficit, substantial oil and gas sector, and ambitious reconstruction programmes create substantial project finance opportunities. However, the legal framework for project finance in Iraq presents unique challenges that require careful navigation by sponsors, lenders, and their legal advisers. This article examines the key legal and regulatory considerations for project finance transactions in Iraq. The Investment Law Framework The primary legal framework for project investment in Iraq is Investment Law No. 13 of 2006 (as amended), which established the National Investment Commission (NIC) as the central body for regulating and promoting investment. The Investment Law provides a framework of incentives for qualifying investments including: exemption from taxes and fees for a period of up to ten years from project commencement; guarantee against non-commercial risk expropriation; right to repatriate capital and profits; and permission to employ foreign workers in technical and managerial positions. Investment Law protections apply to investments approved by the NIC or the relevant regional investment commission. The Kurdistan Region operates under a separate investment law Law No. 4 of 2006 administered by the Kurdistan Board of Investment. Project Company Structure and the SPV Project finance transactions in Iraq typically involve establishing a special purpose vehicle (SPV) a separate project company incorporated specifically for the project. The SPV is the borrower under the project finance loan agreement and the project developer under the project agreements. Under Iraqi Companies Law No. 21 of 1997, project SPVs are typically structured as limited liability companies (sharikat mahduda al-masouliya). Foreign sponsors may hold equity in the SPV, subject to any sector-specific foreign ownership restrictions. The NIC investment licence is typically obtained in the name of the SPV. Key Project Agreements and Their Legal Basis A project finance transaction in Iraq involves a suite of project agreements including: concession or BOT agreement with the relevant government ministry or authority, the legal basis for the project company’s right to develop, operate, and collect revenues from the project; off-take agreement securing the purchase of the project’s output, often by a government entity such as the Ministry of Electricity; EPC contract governing the construction of the project by the engineering, procurement, and construction contractor; O&M agreement governing the operation and maintenance of the project; and government support agreements including direct agreements and support letters from the relevant ministry confirming the project’s legal status and government support. Lender Requirements — Security Package International lenders financing Iraqi projects require a comprehensive security package. Given the limitations of Iraqi security law, the project finance security package typically includes: mortgage over the project’s real property and fixed assets; assignment of the project company’s rights under key project agreements off-take agreements, EPC contracts, and insurance policies; pledge over the shares of the project SPV; assignment of the project company’s accounts including the revenue account, the debt service reserve account, and the distribution account; and direct agreements between the lenders and key project counterparties including the government offtaker and EPC contractor giving lenders step-in rights in the event of project company default. Government Support and Sovereign Risk Government support is a critical element of project finance in Iraq, given the significant role of government entities as offtakers, land providers, and concession grantors. Lenders typically require: a government guarantee or support letter confirming the government’s commitment to the project; a direct agreement with the relevant ministry acknowledging the assignment of project agreements to lenders and confirming step-in rights; and comfort on the government’s obligations under the concession or BOT agreement. Political risk insurance from multilateral institutions such as MIGA (Multilateral Investment Guarantee Agency) or export credit agencies is commonly used to mitigate sovereign risk in Iraqi project finance. International Development Finance Institutions Several international development finance institutions (DFIs) are active in Iraqi project finance, including the International Finance Corporation (IFC), the European Bank for Reconstruction and Development (EBRD), and bilateral DFIs such as the US International Development Finance Corporation (DFC). DFI involvement brings significant benefits: it provides additional comfort to commercial lenders and sponsors on project viability; DFIs typically conduct extensive environmental and social due diligence, reducing reputational risk; and DFI financing may be available on more favourable terms than pure commercial lending. DFI participation also subjects the project to IFC Performance Standards or equivalent environmental and social requirements. How Etihad Law Firm Assists Etihad advises sponsors, lenders, and government authorities on project finance transactions in Iraq. Our services include advising on NIC investment licence applications, structuring project company arrangements, drafting and reviewing project agreements, advising on the Iraqi law security package, negotiating direct agreements with government counterparties, and advising on dispute resolution provisions in project documentation.

Foreign Currency Loans in Iraq

Foreign Currency Loans in Iraq Foreign currency particularly the US dollar plays a central role in Iraq’s economy, driven by oil revenues denominated in USD and the dollarisation of significant portions of the private sector. Yet the Central Bank of Iraq imposes important restrictions and requirements on foreign currency lending that both Iraqi banks and their borrowers must navigate carefully. This article examines the CBI’s foreign currency lending framework, cross-border loan requirements, and the practical implications for structuring USD and other foreign currency financing arrangements in Iraq. The Role of the US Dollar in the Iraqi Economy Iraq’s economy is heavily dollarised. Oil revenues which account for the vast majority of government income are received and managed in US dollars. Large commercial transactions, real estate dealings, and significant portions of trade finance are conducted in USD. The Iraqi dinar (IQD) is pegged to the USD at a rate set and maintained by the CBI. This dollarisation creates both opportunities and regulatory complications for lenders: while USD lending is natural in the Iraqi market, it is subject to CBI foreign currency management requirements designed to maintain the exchange rate peg and control capital outflows. CBI Foreign Currency Lending Restrictions The CBI regulates foreign currency lending by Iraqi licensed banks through a series of instructions addressing: the purposes for which USD loans may be extended, CBI instructions specify eligible purposes for foreign currency lending, typically including import financing, trade finance, and specific investment purposes; foreign currency lending limits banks are subject to open position limits restricting their net exposure to foreign currency assets and liabilities; foreign currency reserve requirements , banks maintaining USD deposits must hold specified reserves; and reporting requirements, banks must report their foreign currency loan portfolios and exposures to the CBI on a periodic basis. Cross-Border Loan Requirements When an Iraqi borrower receives a loan from a foreign lender whether a foreign bank, development finance institution, or international capital market, CBI requirements apply to the cross-border flow of funds. Key requirements include: CBI registration or notification of cross-border loans above specified thresholds; compliance with foreign exchange regulations governing the remittance of loan proceeds into Iraq and repayment of principal and interest to foreign lenders; AML documentation requirements on the source of the lender’s funds; and compliance with sanctions screening requirements particularly given US sanctions implications for USD transactions. OFAC Sanctions and USD Transactions Any transaction involving US dollars including foreign currency loans denominated in USD, is subject to OFAC jurisdiction because USD transactions are cleared through the US financial system. For Iraqi borrowers and lenders, this has direct practical implications: USD lending transactions involving Iraqi parties require OFAC sanctions screening of all transaction parties; any involvement of individuals or entities on the OFAC Specially Designated Nationals list will block the transaction; and Iraqi banks must implement OFAC-compliant sanctions screening programmes as a condition of maintaining US dollar correspondent banking access. The US Department of the Treasury has in recent years taken enforcement action against Iraqi banks for OFAC violations, resulting in the loss of USD correspondent banking access for affected institutions. Practical Structuring Considerations Foreign lenders extending USD loans to Iraqi borrowers should consider: the governing law of the loan agreement, English law is commonly chosen for international loan transactions but Iraqi law implications of security enforcement must be considered; remittance of repayment, ensuring the loan agreement contains mechanisms for the borrower to obtain necessary CBI approvals for remitting USD repayments offshore; security structuring, security over Iraqi assets must comply with Iraqi law regardless of the governing law of the loan agreement; and dispute resolution, international arbitration (ICC, LCIA, or DIFC-LCIA) is commonly chosen to avoid reliance on Iraqi courts for disputes with international lenders. Exchange Rate Risk Management Borrowers taking on USD-denominated loans while generating revenues in Iraqi dinars face significant exchange rate risk. The IQD/USD peg reduces but does not eliminate this risk devaluation of the dinar against the USD directly increases the IQD cost of USD loan repayments. Borrowers should consider: revenue dollarisation where possible, structuring commercial arrangements to generate USD revenues that naturally hedge USD debt service; hedging, limited hedging instruments are available in the Iraqi market; and maintaining adequate foreign currency liquidity buffers. How Etihad Law Firm Assists Etihad advises on the structuring and documentation of foreign currency loan transactions involving Iraqi parties, advises on CBI foreign currency requirements and approval processes, assists with OFAC sanctions compliance in USD transactions, and advises international lenders on Iraqi law requirements applicable to cross-border lending arrangements.

Islamic and Conventional Lending

Islamic and Conventional Lending Iraq’s banking sector operates a dual system: conventional interest-based banking alongside an Islamic banking sector that has grown significantly since the enactment of the Islamic Banking Law. For borrowers and lenders in Iraq, understanding how interest is regulated under both frameworks and the increasingly important role of Islamic finance structures is essential for structuring lending transactions correctly. This article examines the regulatory framework governing interest and profit rates in Iraqi lending, the legal basis for Islamic finance in Iraq, and the practical implications for financing arrangements. Conventional Interest — The CBI Framework In conventional banking, the CBI plays a central role in setting the benchmark for lending rates through its policy rate the rate at which the CBI lends to commercial banks. Commercial banks price their lending based on the CBI policy rate plus a spread reflecting the credit risk of the borrower and market conditions. The CBI monitors interest rate practices of licensed banks and may issue guidance on permissible lending rate ranges to ensure financial stability and prevent predatory lending practices. Under the Iraqi Civil Code, excessive or usurious interest provisions could be subject to challenge a consideration that lenders should bear in mind when structuring high-rate lending transactions. Islamic Banking Law No. 43 of 2015 The Islamic Banking Law No. 43 of 2015 provides the legal foundation for Islamic banking in Iraq. The law permits banks to obtain a licence from the CBI to conduct banking business in accordance with Islamic Sharia principles meaning the bank does not charge or pay interest (riba), but instead uses profit-sharing, cost-plus financing, and leasing structures to generate returns. The Islamic Banking Law requires Islamic banks to establish a Sharia Supervisory Board to ensure that all products and transactions comply with Islamic law. The CBI has issued complementary instructions governing the licensing, operation, and supervision of Islamic banks in Iraq. Key Islamic Finance Structures Used in Iraqi Lending The most commonly used Islamic finance structures in Iraqi bank lending include: Murabaha a cost-plus sale arrangement where the bank purchases an asset and resells it to the customer at a marked-up price, with deferred payment; this is the most widely used structure for trade and asset finance. Ijara, a leasing arrangement where the bank purchases an asset and leases it to the customer, with ownership transferring at the end of the lease term; used for equipment and property finance. Musharaka a partnership arrangement where the bank and customer jointly invest in a project or asset, sharing profits and losses according to agreed ratios; used for project and business finance. Mudaraba a profit-sharing arrangement where the bank provides capital and the customer provides expertise and management, with profits shared according to agreed ratios. AAOIFI Standards and Their Relevance in Iraq The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) publishes Sharia standards that are widely adopted by Islamic financial institutions globally. Iraqi Islamic banks are expected to align their products and practices with AAOIFI standards, which provide detailed guidance on the Sharia permissibility of specific transaction structures. The CBI’s instructions on Islamic banking reference AAOIFI standards as the benchmark for Sharia compliance. For foreign Islamic banks and Islamic finance investors considering transactions in Iraq, familiarity with AAOIFI standards is essential for assessing the Sharia compliance of Iraqi Islamic banking products. The LIBOR Transition and Iraqi Banking The global transition away from the London Interbank Offered Rate (LIBOR) completed at end of 2021 for most currencies has implications for Iraqi banks that reference international benchmark rates in their lending transactions, particularly for USD-denominated facilities. Iraqi banks involved in cross-border lending or participating in international syndicated facilities must ensure that their loan documentation incorporates the appropriate alternative reference rates primarily the Secured Overnight Financing Rate (SOFR) for USD transactions. Existing loan agreements referencing LIBOR should have been amended to incorporate fallback provisions and transition to SOFR or other relevant risk-free rates. Practical Implications for Borrowers Borrowers in Iraq choosing between conventional and Islamic finance should consider: the total cost of financing Islamic finance structures may have equivalent or higher effective costs than conventional lending depending on the structure and market conditions; the regulatory treatment certain CBI requirements apply differently to Islamic and conventional finance; tax implications the treatment of Islamic finance returns under Iraqi tax law should be verified; and documentation complexity Islamic finance transactions require additional Sharia compliance documentation including Sharia board approvals and fatwa opinions. How Etihad Law Firm Assists Etihad advises on both conventional and Islamic finance transactions in Iraq. We assist clients in structuring and documenting murabaha, ijara, musharaka, and mudaraba transactions compliant with CBI requirements and AAOIFI standards, review conventional loan agreements for interest rate provisions, and advise on the LIBOR transition implications for existing Iraqi loan documentation.